If the company makes a trading loss — or has losses left over from earlier years — the Losses section of Corp Tax Calculations is where they're recorded and used.

The four figures

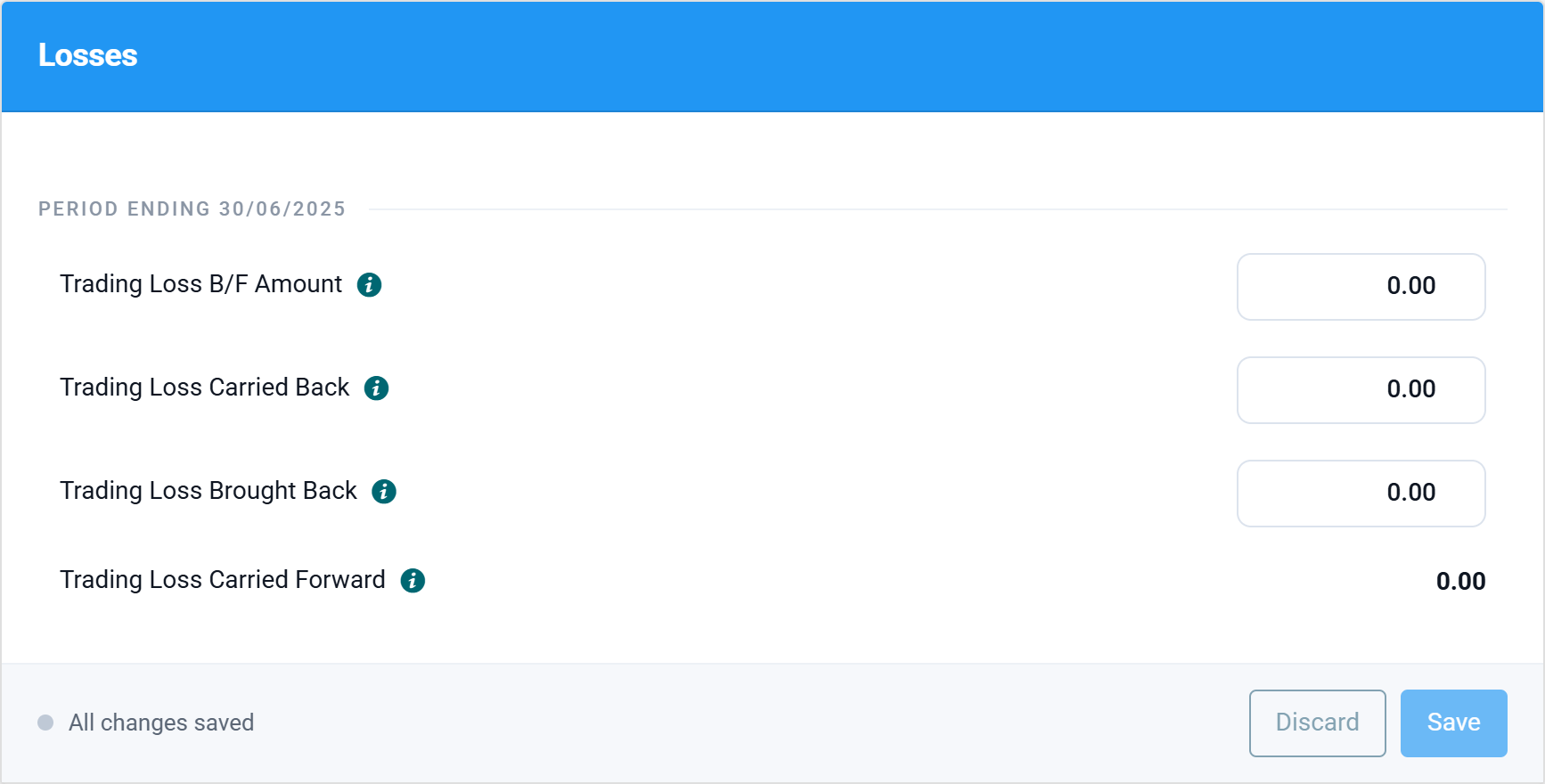

- Trading Loss B/F Amount — losses brought forward from earlier periods. These are set against the current period's profits automatically; post-2017 losses can be used flexibly against total profits.

- Trading Loss Carried Back — if this period made a loss, the amount you're electing to carry back against the previous year's profits (normally up to twelve months). Carrying back generates a repayment of tax already paid, so it's usually claimed before carrying forward.

- Trading Loss Brought Back — a loss arriving into this period from a later loss-making year's carry-back claim. You'd normally enter this when amending a period after a later year's claim.

- Trading Loss Carried Forward — calculated for you: whatever is left after current-year use and any carry-back, available to the next period.

How they interact with the computation

Losses are applied after the trading result and before qualifying donations in the profits-chargeable summary, and the relevant CT600 boxes are populated automatically — including the repayment claim boxes when a carry-back produces one. The computation document shows the loss memo so you (or your accountant) can see exactly what was used, where, and what remains.

A profitable year like the example in this guide leaves the section at zero throughout — you only need it when losses exist.